Finances are Feminist.

Myths, Magic, Capitalism, and the Patriarchy. A YEAR LATER.

Last year I wrote a three part series, not because of my financial know how - but because of what I didn’t know.

I wanted to make some improvements in my overall financial wellness. I made some progress -but not nearly enough.

I moved my savings to a high yield savings account, after it sat there for years with an uninteresting amount of interest. I opened a different kind of checking account that saved me monthly fees and gave me little perks, like free checks. I wouldn’t have known any of these were options, if I didn’t make an appointment to physically sit with a bank teller.

I’ve even tried to listen to a few dude-bro podcasts on investing and finances, but they either left me feeling hopeless because I have yet to invest OR nauseous at the tax avoidance games only the rich can afford to play.

Overwhelmed, I ostriched. Why does this intimidate me so much? Erg.

Now. It’s time to recommit. The cost is too high not to.

All paid subscribers have access to the Financial Planner at the bottom of the post. It’s a full ebook of the process!

Myths at the roots of your money tree

Chances are if you were to take your beliefs by the ankles hang them upside down and gently shake, some money myths would fall out. These are the tiny obstacles that keep you tripping. These are the ones causing you to undermine your value and let your self-esteem get all tangled in the trappings of capitalism.

Ladies, I’m talking to you.

The matriarch in your family was living through a time of limited attitudes toward women and wealth. In one way or another, her beliefs about money set the tone of a story that still echoes in your money myths. They are at the source of your financial wellness.

Before we unravel your own money mindset, let’s dig into the roots of our collective narrative. We still walk the earth with the generations of women who lived this history. This is her story.

History of money and women (HERstory 101)

1848: New York passed the “Married Women’s Property Act”, which permitted married women to own property.

1960s: Women were finally allowed to apply for loans and open checking accounts. It took until 1974 for the “Equal Credit Opportunity Act” (ECOA) to ensure men and women were treated equally throughout the loan process, lenders from then on were prohibited from requiring male co-signers.

1963: The “Equal Pay Act” was established, employers could no longer pay different wages to men and women for the same job. Yet the newest pew center research, indicates women still earn only 82% of what men do.

1972: Congress approved The “Equal Rights Amendment” to federally recognize “equality of rights under the law” for men and women. It took until January 2020 for the 38th state, Virginia, to ratify the amendment. To this date, the amendment has not been formally affirmed - all 50 states do not recognize sex as a legal basis for discrimination. Well, we know how this is going to go.

2007 to 2009 The Great Recession, women were a primary targeted for the predatory loans that would result in the mortgage crisis.

2020: The Census indicates that in the US, women make up only 29% of the those earning a six-figure income.

2022: During the Covid pandemic, women were the most impacted by the need to stay home to provide childcare - either needing to leave their jobs or juggle working from home with home schooling.

2024: Yahoo finance reports 54% of the women surveyed have $500 or less in their savings accounts, while a survey by Brigit, a financial wellness app, showed 30% of women have less than $100 in savings.

Thank you, Raija Haughn for sharing this invaluable data.

The fire to inspire a change for yourself begins with the story of the women who have gone before you. Not only does it spark a responsibility to make a change for yourself, but for the girls who will continue to make their way through the world with this timeline at their back.

Part One: Money Myths: What is at the heart of your relationship with money?

Take a deep dive into your money myth origin story - keep reading the original post.

This can be a tender exercise, but it can shed light on the beliefs you are holding about money, value, and self-esteem.

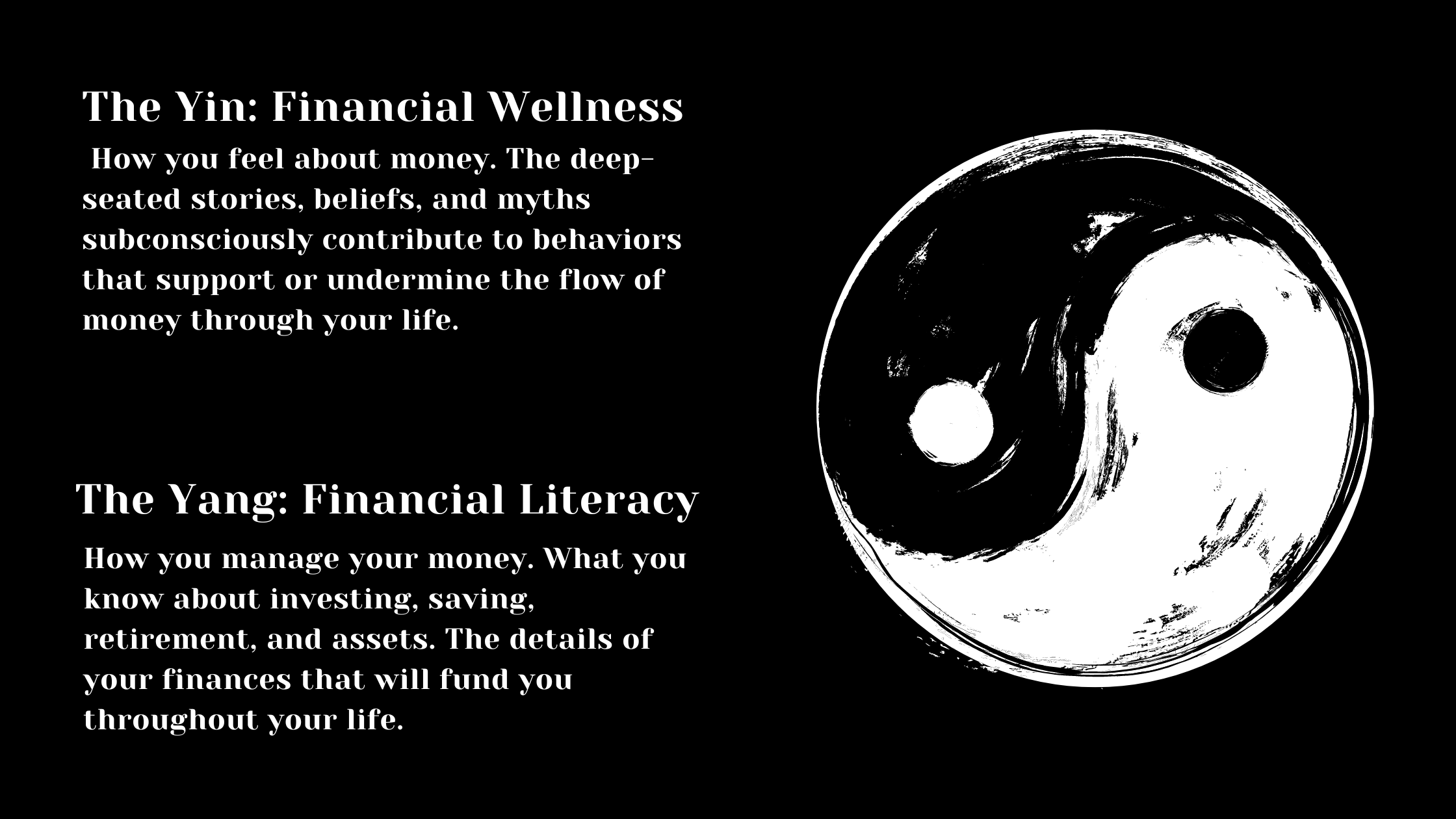

Zen money. The Yin and Yang.

Ken Honda, author of Happy Money, inspired me to approach money in a two fold perspective; Money EQ (financial wellness) and Money IQ (financial literacy). He emphasizes the basis for financial freedom lies in gratitude, trust, and generosity. Riches come alive in our relationships and more vibrant in these invisible assets, without which there is no flow.

In generosity and gratitude, we are more gracious when we pay our water bill for a tap that pours freely. Then acknowledge inequities by contributing to a cause that works to provide clean water to 703 million people without it. With joy, we willingly sacrifice a new sweater to save for a trip that will create lasting memories with our family. And when we pay tuition for a class, we are sending a message of value to our self-esteem that says “I believe in my own potential.”

Financial Wellness: How you feel about money. The deep-seated stories, beliefs, and myths subconsciously contribute to behaviors that support or undermine the flow of money through your life.

Money EQ (Emotional Quotient) - Get clear on how you feel about money and cater to any mindsets that need to heal. It may take a look at your origin stories and money myths to understand the subconscious beliefs that cycle through in this relationship. Any gripping through greed or grasping through worry creates an attitude that breaks the flow.

Financial Literacy: How you manage your money. What you know about investing, saving, retirement, and assets. The details of your finances that will fund your life.

Money IQ (Intellectual Quotient) - The foundation of your wealth comes from your feelings about the green stuff. This informs your saving and spending behaviors, all while weaving through your self-perceptions and your work in the world. This is what you know and understand strategically about your financial goals.

Part Two: Assess your Money EQ and IQ: Is the stagnation through your financial wellness or your financial literacy? Or is it a combination of both?

Assess your Money EQ and IQ: To take stock keep reading the original post.

If we understand that money is a currency, like electricity is a current, we know that it needs to flow to fuel every circuit in our life.

Money Goals, Goals’ Money.

Financial wellness means that you approach your finances with courage and confidence. For many, this is where anxiety tends to seep in. It's okay – most Americans have experienced or currently face debt. Most people are also not earning a six figure income. The important thing is that you go into the details and write them down as neutral facts. In order to get thorough it you’ll need to suspend the inner critic. Seeing the details, is the only way to make a plan of action.

Assess your current financial situation and strategize your goals.

Debt is a four letter word - ignoring it won’t erase it. The big 19 point scrabble word here is- Discretionary (D2I1S1C3R1E1T1I1O1N1A1R1Y4 ) spending. Do I really need one more pair of gauchos? While I'm grateful for credit cards helping me through tight times, my goal is to reduce reliance on them. Instead, it's crucial to build an emergency fund, gradually setting aside money for unexpected life events. Otherwise for non-essentials, learn to save first, spend later.

Reflect on your life goals and incorporate them into your over-all financial plan. Allocate funds toward your short term goals and a savings plan for long term goals. Be realistic about what it will cost you to bring each goal to its success. Get clear on both money goals and goal money. Invest in yourself.

Part Three: 4 steps craft a new financial narrative.

Ditching Debt: Snowball or Avalanche Method.

Short term Budget and Long term Savings.

Connect your financial goals with your life aspirations.

Clarify your wants and prioritize your needs.

Get into the details of your financial situation; plan it out, write it down - keep reading the original post.

The real choice is whether to increase income or reduce spending. The decisions are yours to make. You have the power to manage your money and allocate portions of your income to different facets of your life. The first step is gaining a precise understanding of what holds true importance for you.

This is where you can ditch the spread sheet for a vision board for a minute. Let yourself go there. We all have aspirations that resonate deeply within us, a vision for the life we wish to lead. It’s common to hold idealized versions of our own wealth and imagine how we want it to look, and feel.

This is when understanding your "why" becomes crucial. Why do you seek wealth? Is it for life experiences like trips, dinners with friends, or a ride on a snowmobile? Or do you aim to accumulate possessions like a snowmobile, a house, or a car? Clarify whether your priorities are in living or owning?

The ultimate aim is to get to the end of life with the wealth of health and a unique collection of rich memories.

Your Printable Financial Planner PDF is here 👇.